As 2026 gets underway, crypto markets remain fragmented. Conviction is uneven, risk appetite has yet to fully recover, and many narratives are still searching for traction. Yet beneath the surface, one segment has begun to separate itself from the broader stagnation: real-world assets (RWAs).

This is not a speculative surge driven by short-term catalysts. Rather, it reflects a structural shift that has been building since 2024—shaped by clearer regulatory boundaries, steady institutional participation, and the maturation of on-chain infrastructure. What we are seeing now is the transition of RWA from experimental pilots to early-stage scale.

By mid-January 2026, data from rwa.xyz shows total distributed RWA value reaching approximately $22.9 billion, up from $19.2 billion in mid-November 2025. Growth has been steady rather than explosive. The number of RWA holders increased from roughly 600,000 in mid-December 2025 to about 650,000 by the end of January 202 —an 8–9% rise in just over a month.

More tellingly, monthly active addresses peaked near 100,000 about a year ago and have since moderated, even as total value continues to climb. This divergence suggests that RWAs are increasingly being treated as balance-sheet assets rather than high-frequency trading instruments.

The chain-level distribution reinforces this institutional profile. Ethereum dominates with roughly $13.6 billion in RWA value, accounting for about 60% of the market. BNB Chain follows with $2.3 billion, while Solana and Liquid Network hold approximately $1.1 billion and $1.5 billion respectively. Stellar rounds out the major networks at around $1 billion. Capital is clearly gravitating toward settlement layers that offer predictability, regulatory tooling, and institutional-grade custody. In RWAs, value ultimately concentrates where settlement risk is lowest.

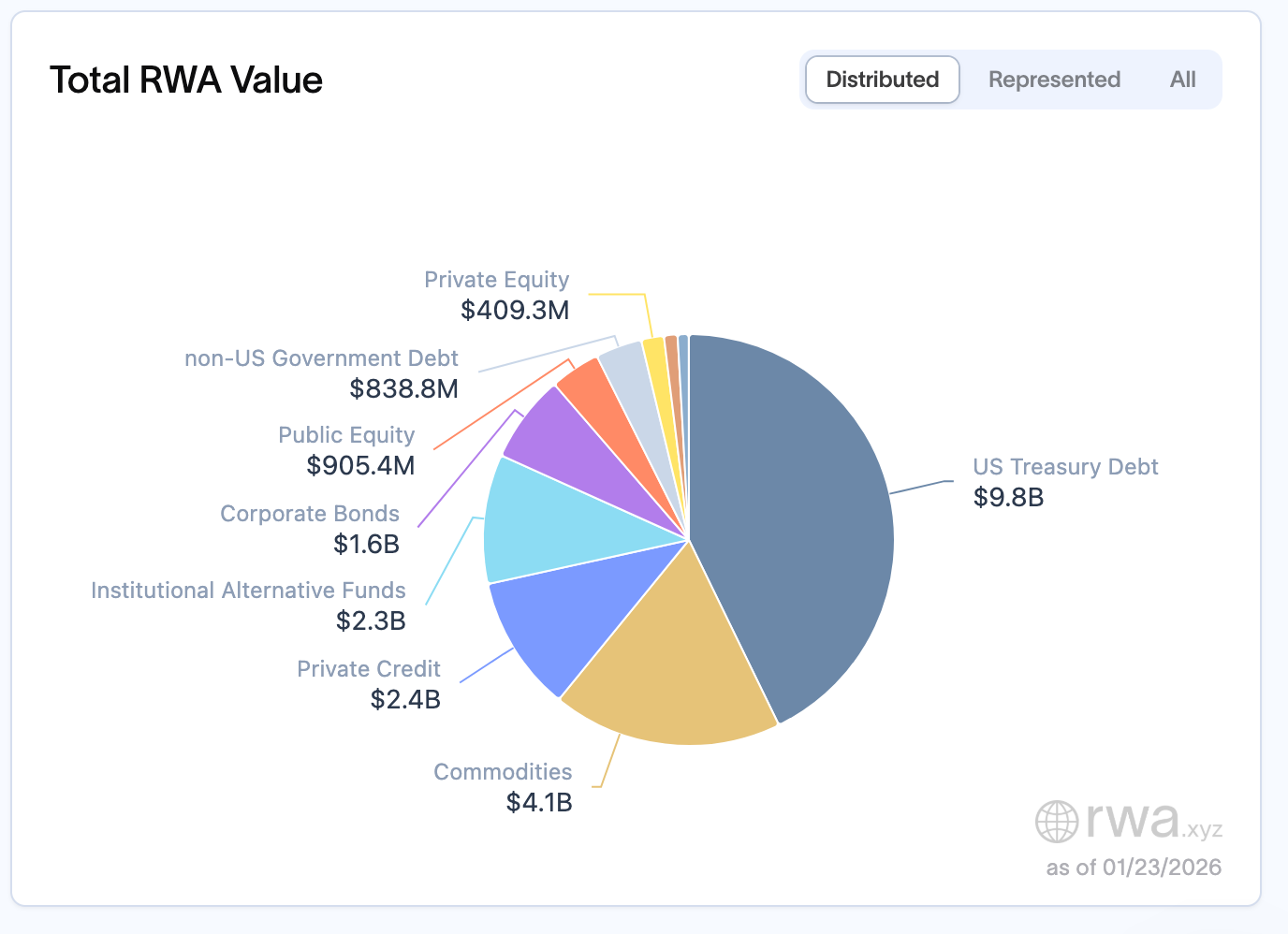

Asset composition tells a similar story. U.S. Treasuries remain the backbone of the market at roughly $9.8 billion, representing close to 45–50% of total RWA value and serving as the primary on-chain entry point for institutional capital. Commodities follow at about $4.1 billion, led by gold-backed tokens such as Tether’s XAUT. Private credit stands near $2.4 billion—smaller in absolute terms, but among the fastest-growing segments. Institutional alternative funds, corporate bonds, and public equities contribute approximately $2.3 billion, $1.6 billion, and $0.9 billion respectively.

This shift was echoed at the 2026 World Economic Forum in Davos, where tokenization emerged as the dominant crypto-related theme. WEF discussions characterized 2026 as a turning point for digital assets, noting that blockchain has moved beyond pilot programs into real production environments. The conversation has evolved from ideology to infrastructure—from whether tokenization belongs in finance to how it can be deployed at enterprise scale.

When RWA Becomes Financial Engineering

Looking beyond headline growth and institutional participation, the composition of today’s RWA market tells a more grounded story. The current wave of expansion is being driven less by productive real-world activity and more by highly financialized assets. In practice, the “real” in real-world assets increasingly refers to legal enforceability and balance-sheet credibility, rather than direct participation in economic production.

U.S. Treasuries, money market instruments, repos, and commodity funds now dominate on-chain RWA issuance. These are not new asset classes, instead, they are core building blocks of traditional finance, with established pricing conventions, predictable cash flows, and well-defined regulatory treatment. Blockchain’s role here is not to transform the assets themselves, but to provide an always-on, programmable settlement layer. As a result, most RWAs today function primarily as low-risk yield instruments on-chain, supporting three main use cases: backing stablecoin reserves, enabling more efficient institutional cash management, and anchoring interest rates across DeFi markets.

At a structural level, this represents an internal efficiency upgrade of the financial system—a migration of familiar assets onto blockchain infrastructure.Of the roughly $22.9 billion in RWAs currently outstanding, U.S. Treasuries account for about $9.8 billion, followed by commodities at approximately $4.1 billion, with gold-backed tokens representing the largest single exposure. Private credit stands near $2.4 billion, and institutional alternative funds around $2.3 billion, while corporate bonds, public equities, and non-U.S. sovereign debt each remain in the $0.8–1.5 billion range. This concentration is no coincidence. Treasuries, money market instruments, and repos align naturally with institutional risk frameworks: they offer transparent cash flows, minimal default risk, well-established valuation conventions, and existing compliance and custody infrastructure. Blockchain’s role here is not to reshape the assets themselves, but to reduce settlement friction and improve distribution efficiency.

These characteristics align closely with institutional priorities. Corporate treasurers are drawn to tokenized Treasuries offering 4–6% annual yields with continuous access, a clear improvement over traditional T+2 settlement cycles. Private credit products typically offer yields meaningfully above traditional fixed-income assets, making them attractive to institutions managing large pools of idle capital. Asset managers use tokenization to lower distribution costs and broaden their investor base, while banks focus on building compliant infrastructure. Together, these incentives reinforce a market structure where financialized assets dominate, further entrenching RWA’s current trajectory.

How RWA Arrived Here

The evolution of RWA has closely tracked shifts in its primary participants. Between 2020 and 2022, the sector was largely shaped by DeFi-native actors, and asset activity concentrated around private credit, trade finance, and SME lending. MakerDAO’s RWA Vaults channeled on-chain stablecoin liquidity to off-chain borrowers, Centrifuge focused on tokenizing receivables and structuring asset pools, and Goldfinch experimented with undercollateralized credit models. This early phase was characterized by elevated yields, higher risk tolerance, and a strong real-economy narrative, focused on bridging crypto capital with small and mid-sized businesses.

A structural turning point emerged in 2023. As DeFi-native yields compressed and stablecoin balances continued to grow, the ecosystem began searching for scalable and durable sources of real yield. U.S. Treasuries proved to be a natural solution. With annual returns in the 4–6% range, near-instant settlement, and continuous market access, they quickly became the preferred on-ramp for institutional capital moving on-chain.

As institutions assumed a more prominent role, the composition of RWA shifted accordingly. Repos rose to dominate represented asset metrics, while private credit receded in relative importance. This was less a change in asset preference than a change in market leadership. When DeFi drove adoption, RWA took the form of private credit. As institutions took the helm, RWA gravitated toward repo-based structures.

Repo’s Success Also Marks Its Limits

Repos have played a central role in RWA’s early growth. Their low risk profile, standardization, and deep liquidity make them easy to integrate into regulated environments, and well suited to serving as the foundation of on-chain financial infrastructure. They support stablecoin reserves, provide reference rates for DeFi markets, and create a familiar bridge between blockchain networks and traditional finance. In this sense, repo has become the financial base layer of today’s RWA ecosystem.

Yet the very attributes that make repos attractive also set clear boundaries on what they can ultimately deliver. Repos do not create new economic activity, nor do they meaningfully expand access to capital in the real economy. Their contribution lies primarily in optimizing existing financial workflows—shortening settlement cycles, improving balance-sheet efficiency, and reducing operational friction. What they enable is a more efficient circulation of capital within the financial system, rather than a reallocation of capital toward new productive uses.

This is not a critique of repo, but a recognition of its role. Repo is indispensable infrastructure, but it is unlikely to represent the end state of RWA. The assets that stand to benefit most from tokenization are not already-liquid financial instruments, but productive assets constrained by illiquidity and rigid financing structures: infrastructure projects, energy assets, compute capacity, receivables, and segments of private credit. These assets generate real cash flows, yet they remain difficult to access due to high minimum investment thresholds and inflexible ownership models. What they need is not higher headline yields, but more efficient and inclusive financing architectures.

Traditional finance struggles most with precisely these types of assets. Physical assets such as solar power facilities and real estate are inherently high in value, yet constrained by rigid, all-or-nothing transaction structures that suppress asset utilization. By enabling fractional ownership, tokenization can materially improve liquidity and help relieve structural bottlenecks in traditional finance.

Ultimately, yield is not the objective; it is the outcome of asset utilization. Repo returns largely reflect prevailing interest-rate conditions, while returns on productive assets are driven by real economic demand. Without utilization, yield becomes artificial and short-lived. For this reason, RWA’s long-term value lies not in making liquid assets incrementally more liquid, but in giving historically illiquid assets their first meaningful access to global capital markets.

Compliance Is Becoming a Feature, Not a Constraint

As institutional involvement deepens, the narrative around RWA is evolving once again. Compliance is no longer viewed solely as a hurdle to adoption; it is increasingly becoming a core component of the value proposition itself.

Since 2025, clearer regulatory frameworks have become an important catalyst for RWA adoption. In Europe, the Markets in Crypto-Assets Regulation (MiCA) came into force at the end of 2024 and continued to enter implementation phases through 2025, providing greater legal certainty for tokenized financial activity. In Asia, Hong Kong introduced several concrete regulatory initiatives in 2025: the Stablecoin Ordinance took effect on August 1, creating a licensing regime for fiat-referenced stablecoin issuers; a new digital asset policy statement released in June outlined support for expanding tokenization, including real-world assets; and regulatory sandboxes and pilot programs have clarified market access and compliance expectations for digital assets. Together, these developments signal a shift from high-level discourse to tangible frameworks that support institutional participation and scalable tokenization.

This shift was evident at Davos 2026, where tokenization was widely described as a turning point for digital assets. The discussion has moved beyond whether blockchain belongs in finance, toward how it will be integrated into existing market structures. BlackRock, BNY Mellon, and Euroclear are already deploying tokenized funds, private debt, and structured products, signaling a transition from experimentation to institutional-scale implementation.

In this environment, structure matters as much as innovation. Assets require robust legal frameworks, market adoption depends on governance, and sustained momentum relies on clear rules. As a result, future token value is likely to be shaped not only by market sentiment, but increasingly by regulatory certainty and operational reliability.

At a deeper level, RWA is not primarily about token issuance. Tokenization provides the rails, but financial design determines impact. Pricing, risk allocation, cash-flow distribution, and governance frameworks matter far more than whether an asset is represented on-chain. Increasingly, the industry is recognizing that RWA is not about moving assets onto blockchain networks—it is about rethinking how capital is structured to reach production.

Toward 2026 and Beyond

Looking ahead, the industry’s direction is coming into sharper focus. On the asset side, attention is expected to shift gradually from purely financial instruments toward productive assets. Compute resources, infrastructure revenue rights, commodities, and energy projects are likely to emerge as the next wave of growth, reflecting a broader move toward assets with direct links to real economic activity. On the product side, the market is beginning to move beyond single-asset tokenization toward structured financing models designed to accommodate different risk-return profiles. At the narrative level, simple yield stories are giving way to a greater emphasis on transparency, governance, and risk disclosure as the primary foundations of investor trust. RWA is also transitioning from isolated pilots to early stages of scale. As minimum investment thresholds decline and compliance tooling becomes more robust, participation is expected to broaden, with holder counts likely to expand meaningfully through 2026.

At the same time, significant challenges remain. Standards for asset verification and continuous auditing are still fragmented, operational risk modeling remains underdeveloped, and secondary market liquidity is limited. Legal frameworks vary widely across jurisdictions, complicating cross-border deployment. From a technical perspective, annual cross-chain transaction costs exceed $1.3 billion, identical assets often trade at 1–3% price discrepancies across networks, and unresolved tensions between privacy requirements and regulatory transparency continue to constrain adoption.

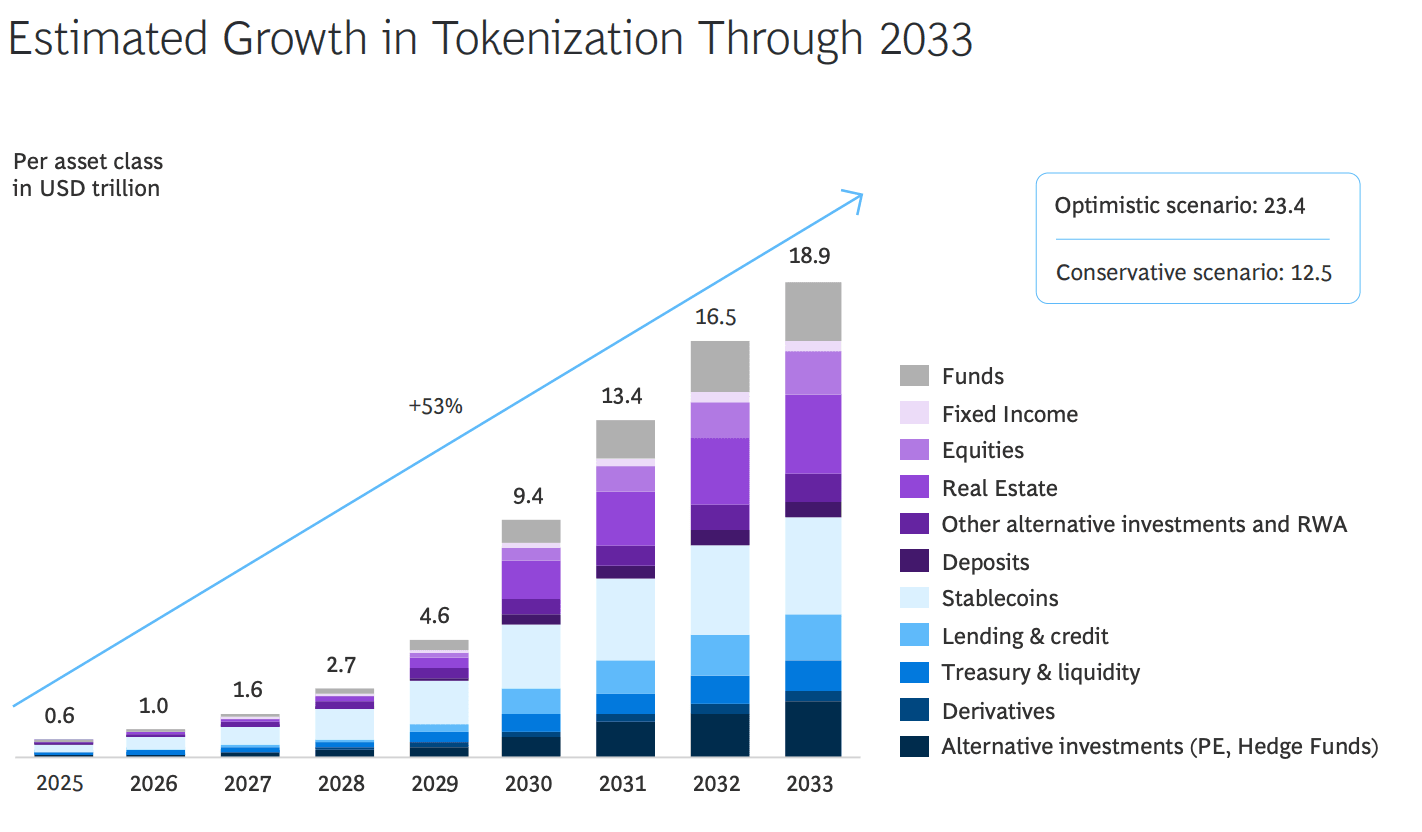

Despite these frictions, the long-term trajectory appears increasingly well defined. Boston Consulting Group estimates that RWA markets could reach $18.9 trillion by 2033, underscoring the scale of the opportunity. Tokenization is no longer framed primarily as a disruptive force, but rather as a form of enduring financial infrastructure.

In this context, RWA’s future will not be determined by headline yields. Instead, it will hinge on how deeply tokenized assets integrate with real-world production and capital formation. Only by grounding itself in the real economy and unlocking liquidity for productive assets can RWA ultimately deliver on its promise of reshaping how capital flows into and supports economic activity.

Connect with us: